Revenue Based Financing: Everything you need to know

Many signposts track the maturing of a startup ecosystem, but one of the most prominent is the emergence of new classes of capital for startups. Equity funding in young, pre-revenue startups may seem run-of-the-mill now in India, but at one point not too many years ago it was revolutionary. As the Indian startup ecosystem grows from strength to strength, new classes of capital have been introduced. A recent one I find exciting for both entrepreneurs and investors is Revenue Based Financing and that’s what I want to talk to you about here.

ALTERNATIVE FINANCING

But before that let’s make some clear classifications, because many of the capital classes may seem similar at first glance. At its simplest, in startup financing, equity funding confers ownership to the investor to the extent of his or her shareholding. This translates to high risk and high reward —if the startup doesn’t work out, an investor might not get even his capital back, but there is potential for a multibagger if the startup becomes a spectacular success. The recent DoorDash and Airbnb IPOs are great examples of the latter, with multiple

venture capital investors seeing stellar returns and exits. Softbank Vision Fund, for instance, converted a $680 million investment in DoorDash into an $11.5 billion return. Sequoia, on the other hand, invested about $280 million over multiple rounds in Airbnb and its stake on the company’s listing was valued at an impressive $12 billion. The returns are said to be even more impressive for YCombinator, which was an early investor in both companies. But the accelerator has not revealed exactly how much it has made. In India, the Happiest Minds IPO also provided a stellar 40%-plus IRR in five years for investor JPMorgan when the company went public in 2020.

Traditional debt, on the other hand, is low-risk-low-reward and does not provide ownership for the capitalprovider. The startup/entrepreneur needs to pay back this debt with a prefixed interest in a set period of time. If the startup does not work out, debt takes precedence over equity in terms of returning the capital.

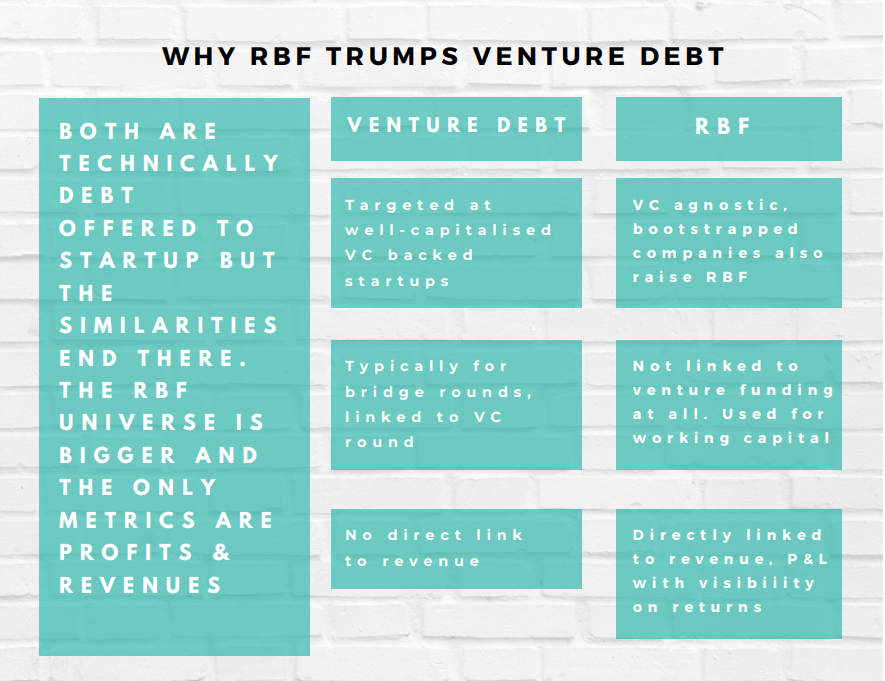

For entrepreneurs looking to raise capital without diluting too much of their equity, venture debt became a strong source of capital. While venture debt has been around in India for over a decade, it has become more popular among startups in recent years. India recorded over $427 million worth of venture debt deals in 2020, according to data from Inc42. Venture debt is offered to startups that have already raised at least one round of venture capital funding and is a medium-term loan with fixed interest rates with monthly repayments. In a way, venture debt is an extension of equity funding. Significantly, there is no typical collateral backing the debt; instead, the company’s warrants are used, with the option to convert the warrants into equity over a period of time. Warrants are the deal sweeteners.

Revenue Based Financing (RBF) is a new form of capital that is gaining popularity in mature ecosystems like the US but is a pioneering asset class in India with investors beginning to test the waters only now. So, what really is RBF? I would classify RBF as a hybrid product with medium risk and better than debt returns.

Here are some key points:

- It is a debt given to the startup, but not structured as a loan.

- Like its name suggests, investors get a fixed percentage share of the business’ revenues each month. So if a company has higher revenue one month, the investor gets a greater share back. This repayment covers the principal plus a return that is decided at the time of investment.

- This is typically meant to meet working capital requirements. The founders do not have to dilute equity, which makes it attractive for them, and hence a ready market is available to interested lenders

- There is no hard collateral or guarantees backing the financing, so it is higher risk compared to secured loans for investors/lenders. In addition to risk mitigation and control mechanisms available to lenders, RBF wherever feasible provides a right to the startup’s Intellectual Property and/or movable assets.

RBF PICKING UP STEAM

For companies that can reliably predict their revenue flow, this type of alternative financing is a highly attractive prospect. This is why globally, online businesses and SaaS companies particularly are increasingly opting for RBF. These startups, while not necessarily profitable do have a regular revenue stream.

For the entrepreneur the advantages are clear, they do not need to dilute their equity, there is no collateral involved. Further, since the payment is linked to revenue, repayment does not become a strain.

WHAT’S IN IT FOR INVESTORS?

Investors typically have a clear asset allocation across public markets, private equity, debt, and alternative assets, which is perfectly fine. But many of you are looking at better balancing or diversification of your portfolio within each asset class, and RBF offers an answer. RBF does not replace venture or equity investment in your portfolio. With RBF, the core premise of the product is the strength of revenue and quality of revenue of the startup you are providing funds to. Here the key is that the return is directly linked to a company’s revenues over the next two to four years. Alternatively, return on VC investments typically takes eight to 10 years.

With estimated returns of 20% plus, RBF offers an opportunity to better the overall yield of an investor’s debt portfolio, which is always good news. Apart from this, only a handful of companies raise venture capital funding and of these only a few will bring that 50x return that makes for a blockbuster exit. The universe of revenue-earning startups is much bigger. Not all of them are attractive from a VC point of view, but are great from an RBF perspective. The larger pool of potential investee companies is in itself a big win for the investor and the founders.

Author

More in:Capital Call

Subscribe to our Blogs |